A lot of the stuff on the wiki and site is massively simplified and not strictly true. If you don't know much about finance, stuff like "return is always associated with risk, there is no free-lunch" is a good place to start, but more knowledgeable and quantitative investors know that this isn't true (according to CAPM, only systematic risk generates return, not specific risk).

If you haven't thought much about what kind of volatility you are okay with and aren't really interested in managing your money, a boglehead kind of portfolio is good place to start. It's something, for example, that I might recommend my mom, if I wasn't willing to put in the work to manage her investments for her.

But for a technical crowd, like HN, the stuff on the site misrepresents modern financial theory and perpetuates people saying stuff that doesn't even make any sense, like, "you can't beat the market", "don't hold a leveraged index fund", "active management is a scam", etc. Like all things people say, these have a kernel of truth, but the specifics and context are so far removed that these statements become meaningless, or even flat out wrong.

Even by just holding simple, automated ETFs (I don't call this passive investing, because passive investing doesn't exist), there's tons of room for really interesting optimizations that increase return and decrease risk. Things like risk parity portfolios, minimum variance optimizations, persistent factor portfolios, etc.

And best of all, with zero commissions, super tight bid-ask spreads, and easy to access APIs, "quant-lite" investing is more accessible than every before.

In conclusion, every portfolio is an active portfolio, from deciding a equity/bond ratio, to investing in real estate, to deciding to buy some TSLA. It's all the same, so stay away from any dogmatic approaches to investing (I would say the bogleheads are pretty dogmatic). By becoming familiar with the biggest and most important advances in quantitative finance, along with understanding your own risk tolerance, you can construct a portfolio that is perfect for you, and that will give you so much more than a one-size-fits-all boglehead portfolio could ever hope to.

I don’t know your background. But I’ve worked at an investment bank the past 15 years and have traded every kind of stock, bond and derivative there is.

With respect, you sound a little bit like every new programmer that I’ve worked with. They get a taste of learning about finance and suddenly become day traders. They make some money and then suddenly they give it all back and more because they really weren’t understanding what they were doing.

In general, anyone with a full time job that thinks they can out-compete full time traders that specialize in the exact instrument that you are trying to trade will have a very expensive lesson some day.

If you really want to pursue it at least take the level 1 CFA exam. If you can’t pass that you don’t have much of a chance and if you can pass that you’ll probably realize you don’t want to do it.

Could someone with your experience help me on where to get started if I want an in depth knowledge of the kind of stuff you use on a day to day basis? Would preparing for and writing the level 1 CFA be a good start? (I'm a mathematical physics graduate who's done quite a bit of software in finance but not specifically in trading).

I've read quite a bit of quant material, but I would also like to know what to learn from someone who is steeped in the industry as I'm sure my knowledge is quite a rough approximation of what I should actually know if I were to claim any expertise.

CFA Level 1 official prep material is very good. IIRC, these are set of 6 books. You can get second hand older prep material from eBay/Craigslist/FB for cheap.

> “ In general, anyone with a full time job that thinks they can out-compete full time traders that specialize in the exact instrument that you are trying to trade will have a very expensive lesson some day.”

I hear this a lot and it’s definitely something I would expect to be true. But I’ve been repeatedly surprised that it’s not.

I’ve made a lot investing on the side (usually just stock, sometimes calls - recently for peloton in January, stock for tesla in 2012 which I sold early last year before the crazy recent rise, stock for Apple, Amazon, Nvidia, Facebook, AMD).

Am I stupid, lucky or both?

Yes longest bull run in history, but investing in large tech companies you think are stable long term with good CEOs when you know the field (Apple, Amazon) seems pretty easy.

When you read a lot of comments from traders on the east coast they seem like they misunderstand the companies, or are not focused on long term strategic moves.

I’m mostly positioned in total market index funds with a couple large positions in companies I think will continue to outperform long term, but it doesn’t seem that hard to do better than traders.

Plus the index funds contain a lot of companies I would never personally invest in if they weren’t in the fund, still good to hedge against my own (likely) arrogance.

I did sell each of them after while (once I got long term capital gains and needed the money for something else or wanted to move to a different stock).

So day traders no, but other traders yes? Particularly the peloton calls (2yr expiration leaps) were an explicit trade against some industry person that was extremely wrong.

I used to work in finance doing portfolio analytics. I'm not really advocating day trading, but rather using quantitative methods for optimal portfolio construction.

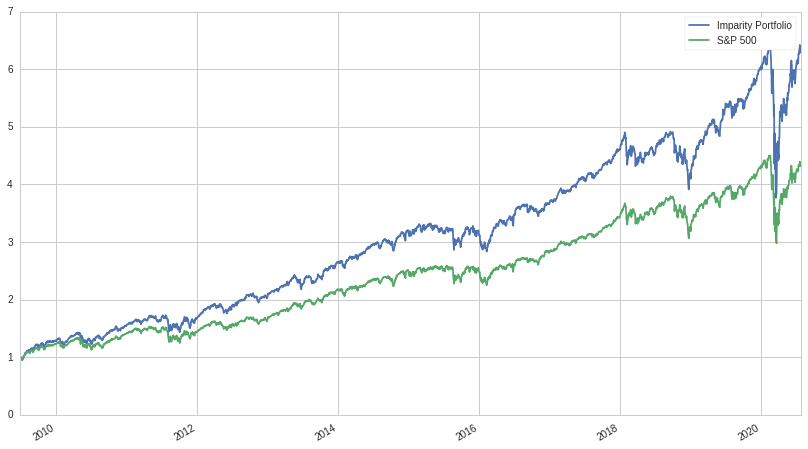

>For example, if we purchased a 2x bull leveraged S&P 500 ETF such as SSO, we would choose an appropriate weight to cancel out the leverage, 0.5 in this case. If we kept the rest of the money in cash, the return of the portfolio would only be slightly worse than that of the S&P 500, due to the 0.90% expense ratio we pay.

A 2x bull leveraged etf replicates daily moves. your long term return to expense expectations are completely off.

You are exactly correct. So many people are buying these synthetic instruments without even reading the prospectus that clearly states in plain language what you said but they still buy them expecting > daily tracking.

I’ve seen so many strategies that technology people come up with (including myself) that look great on paper but don’t take into account the prospectus or things like market conditions, counterparty risk, backwardation, contango, etc.

You're right that 0.9% is a lot, but the expenses get absorbed by the bond yield. The total difference of return between 0.5*SSO and SPY over the ten year period (2010-01-01 and 2020-01-01) is 28%. Maybe you're right that that's more than "slightly" worse, I'll change the wording.

Moreover, when doing at the historical returns, I do use UPRO, not just 3xSPY, so the expense ratio is included. It's not included in the chart that goes back to 2004, but I do mention that that one is synthetic and inaccurate.

Its not labeled on the axis. But the analysis is up to last Friday. It's also easy to see that the huge drop and rebound at the end of Coronavirus. The start and end date are also mentioned in the post.

> return is always associated with risk ... this isn't true ... only systematic risk generates return

On the contrary, your criticism that "only systematic risk generates return" does not invalidate the assertion that "return is always associated with risk". Perhaps you misinterpreted the direction of causality implied by that assertion, thinking that it meant risk is always associated with return?

You can take on more risk and not get any more return. Conversely, you can get more return and not take on anymore risk. That's like the foundation of Modern Portfolio Theory.

Theory tells us that you can't get more return without taking on more risk, if the market is efficient.

Of course, the market can't be perfectly efficient, but it's possible that the market is weakly efficient: the cost of information is so high that it, on average, makes it impossible to beat the market.

No, only if the portfolio is on the efficient frontier. There are many sub-optimal portfolios that do not have the best return/risk trade-off, like portfolios with a lot of specific risk. Check out the Markowitz Bullet.

Specific risk does not get compensated because it is easy to eliminate it with diversification.

I should have been more specific (no pun intended). You should take a closer read of my comment. You've made the same misinterpretation a second time.

Suppose a non-diversified investor, A, owns an asset which has both systemic risk and specific risk, and a diversified investor, B, has the same knowledge as A. In this case, B would be willing to pay a higher price for the asset than A would. A then sells the asset to B and the market becomes efficient. No assets would exist not on the efficient frontier.

You can, but not consistently according to the Efficient Market Hypothesis. If you are referring to e.g. factor investing, that's not "beating the market" in the traditional fund manager way, just holding it differently and taking more systemic risk for a higher potential upside (if the factor is indeed based on risk and not irrationality of market participants).

> And best of all, with zero commissions, super tight bid-ask spreads, and easy to access APIs, "quant-lite" investing is more accessible than every before.

I'm conservative here and would wait 10 years before jumping on some fancy new technique to make more money. Why? Because fin history is littered with fancy new ways of making money that primarily made the manager money. Any real advantages are going to be quickly taken up by competing money makers anyway.

> In conclusion, every portfolio is an active portfolio, from deciding a equity/bond ratio, to investing in real estate, to deciding to buy some TSLA. It's all the same, so stay away from any dogmatic approaches to investing

This is dangerously wrong advice. "Passive investing" in the Bogleheads sense and choosing e.g. a equity/bond ratio is based on science and 120+ years of available data (Efficient Market Hypothesis, Modern Portfolio Theory), buying TSLA is not. Real estate is a very mixed bag (for US research, see e.g. Beracha et al. 2012 "Lessons from over 30 years of buy versus rent decisions" in Real Estate Economics Vol 40 No 2, and https://www.prnewswire.com/news-releases/house-of-cards-morn...).

Conclusion: the "dogmatic" approach is absolutely the right thing for 99% of retail investors to follow.

During the same time, bonds sold off too. Everything did.

If you were dollar cost averaging into the market for 12 years, you could find yourself below where you started. That's a pretty demoralizing situation.

I think being aware of market conditions and reallocating as you see fit is just part of being a responsible adult. Maybe sometimes you do want to hold VTI, but also it's not unreasonable to bet on Elon.

I'm not saying everyone has to be highly leveraged and aggressive, but I think you're putting a tremendous amount of faith in the markets and intentionally looking the other way.

This does not account for dividends, which, if reinvested, would have produced a 22% gain during this time period, which is not too bad when "everything was selling off"

Not spectacular, but you also need to compare this to whatever alternate investments you would have chosen at that time, and would have kept until now. Gold, Cash, small caps, real estate, multi-factor, managed futures, ?

You also need to consider why you have chosen these to points in time.

Looking backwards, there were probably better things to do with your money during that specific time period, but would you have chosen them in 1996 ? And would you have kept them until today ? And, if not, would the changes you would make have also done well ? You would need to be right in both investment selection and timing many times to have done better than the SP has done.

I wasn't accounting for reinvested dividends, but inflation from 1997 to 2009 was 34%.

I'm choosing those points because I remember hearing from retirees in 2008 that they had followed all of the advice and they are worse off than they were 10+ years ago. I saw too many cases of people being upside-down on their mortgages, while losing their jobs, while losing their retirements. In that situation, it's pretty hard to keep saying "don't worry, it'll come back, just keep dollar cost averaging in". If you were retiring in 2008, you might not be able to keep averaging with the market, even if you had the stomach to do it. Time in the market is still timing the market.

We've only had modern portfolio theory since 1952. In the last few decades, we've done some really experimental monetary policy. I won't be shocked if we experience some event that brings us back to 2008 levels. I also won't be shocked if we see hyperinflation. The one thing I know is that you're always trying to time the market, it's just a question of if you acknowledge it or not.

I think it's a good idea to max out your tax-advantaged retirement plans and dump them in indexes as sort of a safety net because your MPT advice is probably "too big to fail" at this point, but that only accounts for less than 20k/year of investment advice (for most employed people). After that, investing in a residence makes a lot of sense because of the tax advantages. If you happen to be in a situation where you can engineer more tax advantages (like owning a business or moving to a lower-tax state), then definitely do that. Once you've got all that sorted, it's pretty much just gambling.

> If you were retiring in 2008, you might not be able to keep averaging with the market, even if you had the stomach to do it.

That is why you need to risk-adjust your portfolio before you hit retirement and see to it that you have other assets to fall back on in case of market implosions. Landing in a ditch with your stocks as the only possible income during 2008 means your assessment of your risk tolerance was wrong and you found that out the hard way. Staying in stocks means accepting the risk that things go south in exchange for high potential returns. As we saw, the markets climbed back (I think the average is 2-3 years of misery in past crises before it gets back up) and had a 10-year bull run before Corona hit.

A fully paid off house can help sit out crashes, too, sure. Investing in stocks while still paying your house off, well... some people like to live on the edge :-)

> Time in the market is still timing the market.

No. Timing the market is making decisions in between about getting in and out for other things than rebalancing, adjusting your risk or for some rational tax purpose.

As mmmrk responded, you need to settle on a risk profile.It is not all or nothing.

You should assume the "market" will go down 50% at any given time, and ask yourself how that would effect you. You need how much to keep in "safe" assets, such as quality bonds and/or cash.

If you are retired and your assets drop in half, will you be ok ? If not, reduce equity exposure until you reach a point where you will be ok.

I aim to own my house outright, and have no more than 50% in equities. That's me, that's my risk tolerance. If the market goes down by 50%, I am still fine, from a financial perspective. So I would not feel the need to sell in a panic. If I had a large mortgage, all stock, I would probably panic.

Owning a business, imo, is much riskier. You can go out of business and also end up in debt. Imagine if you owned a bunch of restaurants right now.

Again, what is the alternative ? Managed futures, minimum volatilty, small cap, factors, oil rigs, private equity - none of these have shown to work when the st hits the fan. Maybe gold.

And on other dates, it was not $773. So what? Long term, the world market (more than the US) historically averaged to 6-8% growth p.a. with dividends before inflation iirc, and the last 120 years were certainly no walk in the park for the world. If you look at the MSCI World in the past 30 or 40 years, you would have made no loss in any time window if you bought and held at least 15 years. The key is time in the market. 12 years isn't much. Think 20, 30+ or until you die. Psychological pain in downturns is the price you pay for far superior returns in the long run to any other asset class.

Switching between VTI and single shares is market timing and therefore gambling. If you want to reduce the maximum drawdown, ramp up the allocation of less risky assets like bonds or cash on a savings account.

While I largely agree with your post, you are forgetting about the total return, yes the S&P was like for like on a net basis, but dont forget about dividends in the intermediate period.

there's obviously a lot of folks here who aren't "technical", see endless stream of "how to find a technical cofounder"-esque posts. (and that's ok!)

and even the engineering school and math grads floating around on here can't be expected to have significant financial expertise.

> If you haven't thought much about what kind of volatility you are okay with and aren't really interested in managing your money, a boglehead kind of portfolio is good place to start.

that's most people! even on HN!

> By becoming familiar with the biggest and most important advances in quantitative finance

i'd love to see a summary or jumping off point for this.

But the "you" here isn't you, it's people who aren't hobbyist investors (let alone professionals). People who don't know, and don't really want to know, what "risk parity" or "minimum variance" is. I don't think any boglehead truly believes nobody can beat the market.

{kind=link}

If you haven't thought much about what kind of volatility you are okay with and aren't really interested in managing your money, a boglehead kind of portfolio is good place to start. It's something, for example, that I might recommend my mom, if I wasn't willing to put in the work to manage her investments for her.

But for a technical crowd, like HN, the stuff on the site misrepresents modern financial theory and perpetuates people saying stuff that doesn't even make any sense, like, "you can't beat the market", "don't hold a leveraged index fund", "active management is a scam", etc. Like all things people say, these have a kernel of truth, but the specifics and context are so far removed that these statements become meaningless, or even flat out wrong.

Even by just holding simple, automated ETFs (I don't call this passive investing, because passive investing doesn't exist), there's tons of room for really interesting optimizations that increase return and decrease risk. Things like risk parity portfolios, minimum variance optimizations, persistent factor portfolios, etc.

And best of all, with zero commissions, super tight bid-ask spreads, and easy to access APIs, "quant-lite" investing is more accessible than every before.

In conclusion, every portfolio is an active portfolio, from deciding a equity/bond ratio, to investing in real estate, to deciding to buy some TSLA. It's all the same, so stay away from any dogmatic approaches to investing (I would say the bogleheads are pretty dogmatic). By becoming familiar with the biggest and most important advances in quantitative finance, along with understanding your own risk tolerance, you can construct a portfolio that is perfect for you, and that will give you so much more than a one-size-fits-all boglehead portfolio could ever hope to.